Can the Nigerian Informal Economy Survive Without PoS Operators? They Are Threatening a Nationwide Service Suspension

PoS operators in Nigeria are threatening a nationwide service suspension over alleged monopoly practices by Verve International and Interswitch, exposing growing tensions in Nigeria’s digital payments ecosystem and the fragility of the informal economy that millions of Nigerians depend on daily. Can the Nigerian economy survive without PoS operators?

Most informal business men and women, in their daily bid to survive, do not have a banking app. Some do, but rarely use it. Most simply have a debit card tucked carefully away in a wrapper, wallet, or some other safe place, and it only comes out when they need to withdraw cash.

Take Mama Chisom, for instance. She runs a small provision shop on a street corner in Onitsha. Every morning almost like a ritual now, before opening for the day, she walks two minutes to a nearby PoS operator, withdraws ₦5,000, and starts work.

She does not queue at an ATM or wait for cash to be loaded. She does not need to visit a bank branch. She simply walks, withdraws, and gets on with her day.

That two-minute transaction is the product of an entire financial ecosystem that most Nigerians rely on daily, yet almost nobody thinks about until it stops working. Right now, it might be on the verge of doing just that.

How the PoS Economy Was Born Out of a Policy

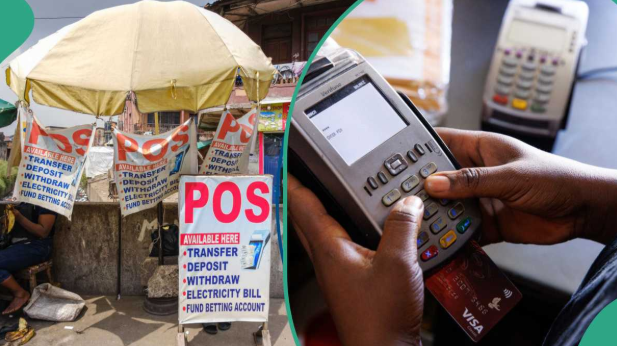

The Point of Sale terminal did not organically become Nigeria's most widely used financial touchpoint, it was pushed into that position.

The Central Bank of Nigeria's cashless policy, which began rolling out in phases from 2012 and intensified significantly between 2022 and 2023, deliberately reduced cash availability to encourage Nigerians to embrace digital payments and agent banking.

ATM withdrawal limits became tighter. Access to cash through bank branches became more restricted. Then came the 2023 naira redesign exercise, which triggered an acute cash shortage that even ATMs could not adequately address.

As cash became harder to access through traditional channels, PoS operators emerged as the most reliable source of cash for millions of Nigerians.

It was into this vacuum that PoS operators stepped in and gained widespread significance. The terminal, which had existed quietly since the mid-2000s, suddenly became critical infrastructure in the Nigerian economy and for Nigerians.

Fintech companies such as OPay, Moniepoint, and PalmPay poured into the agent banking space, onboarding operators, reducing terminal costs, and building the distribution networks that placed a PoS machine within walking distance of almost every Nigerian neighbourhood.

By the first eight months of 2025 alone, PoS transaction value on the NIP platform had exceeded ₦88 trillion. By Q1 2025, there were more than 5.9 million active PoS terminals across the country, up from 2.6 million in March 2024.

That is not simply organic market growth. It is the direct consequence of policy decisions, a reality that few people are being completely honest about.

What the Operators Are Actually Saying

The Association of Point of Sale Service Providers has warned that it may direct members nationwide to suspend the acceptance, processing, and switching of Verve card transactions over what it describes as exclusivity practices in the market.

The threat is directed squarely at Verve International and its parent company, Interswitch Limited. According to the Association, unless the Central Bank of Nigeria (CBN) and the Federal Competition and Consumer Protection Commission (FCCPC) intervene, PoS operators could halt Verve-related services across the country.

The Association argues that four specific issues have made the threat of suspension unavoidable:

1. Verve and Interswitch maintain an exclusive monopoly over the processing of Verve card transactions, which the Association argues restricts competition within Nigeria's payment ecosystem and shuts out rival processors.

2. The two companies are accused of abusing their dominant position in the domestic card scheme market, in alleged violation of Section 72 of the Federal Competition and Consumer Protection Act 2018 and CBN Guidelines on the Operation of Electronic Payment Channels.

3. Interswitch and Verve are allegedly imposing scheme fees that exceed the acquirer's regulated share of the Merchant Service Commission, meaning PoS operators are paying more than the CBN's own rules allow.

4. The Association alleges illegal and unauthorised debits on settlement accounts belonging to acquirers, processors, and switches, essentially claiming that funds are being pulled from accounts without proper regulatory approval.

The Association has formally written to both the CBN and the FCCPC. The threat is not a walkout over wages or workplace conditions. It is a regulatory complaint with commercial teeth, and the weapon they are threatening to use is a nationwide service suspension that would affect merchants, consumers, financial institutions, and thousands of SMEs in one move.

The Person Nobody Is Talking About

The regulatory language in this dispute is dense. Merchant Service Commission. Acquirer share. Settlement account debits. Dominant position abuse. None of that vocabulary reaches Mama Chisom.

What reaches her is the outcome, if PoS operators suspend Verve card processing, and Verve is Nigeria's largest domestic card scheme by volume with over 50 million cards in circulation, the ripple hits every Nigerian who carries a Verve card, runs a PoS terminal, or relies on agent banking for their daily cash needs.

This is the part of the conversation that consistently gets swallowed by the institutional framing. Nigeria's informal economy, the suya seller, the kiosk owner, the dispatch rider, the market woman, was not designed around banking infrastructure. It was pushed toward it.

The CBN's cashless policy was not a consultation with informal traders; it was a policy rolled out at the top that reshaped behaviour at the bottom. Those people adopted PoS not because they understood the payment ecosystem but because the alternative, standing in a bank queue for thirty minutes only to be told the system is down, became increasingly untenable. They adapted and now the system they adapted to is having a dispute above their heads.

Why There Are So Many Terminals and So Little Stability

The density of PoS terminals in Nigeria is both an achievement and a symptom. It's an achievement because financial access expanded rapidly, rural communities, underserved urban neighbourhoods, and low-income earners who never had bank accounts are now participating in the digital economy through agent banking.

The numbers actually confirm it: active bank accounts hit 320 million by March 2025, up from 311.6 million at the end of 2024, with much of that growth driven by fintech-led onboarding at agent banking points.

But the density is also a symptom of a system that scaled faster than its regulatory architecture could keep up with. The same CBN that mandated the cashless policy is now being asked to adjudicate a dispute between the operators that created the policy created and the card scheme that powers most of those terminals.

In late 2025, the CBN also introduced a regulation restricting each PoS agent to a single terminal per network operator, a rule that PoS operators protested as threatening their livelihoods. The sector is simultaneously expanding and being squeezed from multiple directions at once.

What nobody is saying is that Nigeria built an informal financial layer on top of a formal infrastructure that was never stress-tested for the load it is now carrying, in volume, in complexity, or in the number of ordinary Nigerians whose daily economic survival depends on it functioning correctly.

What a Suspension Would Actually Cost

A nationwide PoS suspension would not look like a financial crisis in the newspaper sense. There would be no market crash, no exchange rate spike, no emergency press conference from the Minister of Finance.

What it would look like is Mama Chisom being unable to withdraw her ₦5,000. A trader in Aba unable to receive payment at his terminal. A 9-to-5 worker in Lagos searching for cash for transport, hoping to avoid friction with drivers.

A rural community where the nearest ATM is forty minutes away, and the PoS operator, its only accessible financial point within walking distance, suddenly has no functioning financial access at all. The damage would be absorbed quietly by the people least equipped to bear it.

The CBN and FCCPC have the tools to intervene and the mandate to do so. The Association has escalated formally and publicly. Whether the institutions move fast enough, or at all, before operators act on the threat is the only question that matters right now.

Because the PoS operator sitting under an umbrella with a phone strapped to a terminal is not just a micro-entrepreneur. They are, for millions of Nigerians, the closest thing to a bank branch that actually works.