Kenya Is Seeking $774 Million From the IMF And Running Out of Room to Absorb Another Shock

Kenya is seeking fresh IMF and World Bank support to manage rising fuel prices and economic pressure from Middle East tensions. But as the country returns to multilateral lenders again, the deeper question is whether Africa's debt-dependent economies can ever break the cycle.

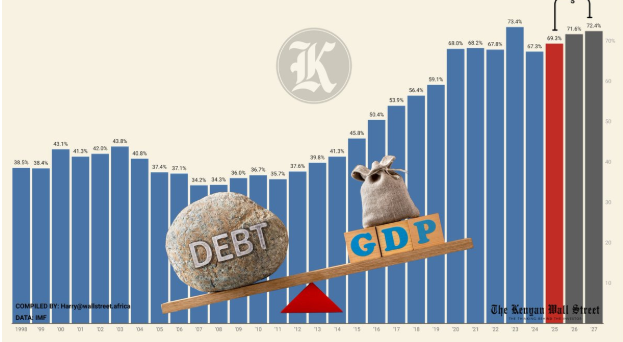

The Kenyan government did not arrive at this moment by accident. For the better part of the last decade, the country has been running a fiscal strategy built on external borrowing, optimistic revenue projections, and the quiet hope that growth would eventually outpace the debt but it hasn't.

In 2024, Kenya's public debt had crossed KSh 10 trillion, and the government was spending more on debt servicing than on health and infrastructure combined. The economy kept moving, but the room to manoeuvre kept shrinking.

Now, with Middle East tensions driving global fuel prices upward, Nairobi is back at the table, this time seeking a fresh International Monetary Fund (IMF) programme worth approximately KSh 100 billion, roughly $774 million, to cushion the country against the latest external shock.

The Treasury Cabinet Secretary confirmed the talks on Monday, 11th May. The IMF had already revised Kenya's growth forecast downward from 4.9% to 4.5%, citing inflation pressures and geopolitical risks tied to the Iran conflict.

This is where things stand. The question worth asking is how many times the same cycle can repeat before the structure underneath it gives way.

The Debt Architecture Kenya Built and Now Lives Inside

Kenya's borrowing did not happen in one dramatic decision. It accumulated across administrations, each with defensible reasons at the time, infrastructure gaps, revenue shortfalls, COVID-19, drought, and now a global fuel shock with origins in a conflict Kenya has no part in and no control over.

The IMF's standard programme architecture is familiar by now. Funds arrive in tranches and each tranche is tied to specific reform benchmarks. Those benchmarks typically include fiscal consolidation, revenue targets, and subsidy rationalisation. Countries reform first, then the money follows. Kenya has been through this process before and knows what the fine print looks like.

What makes this round different is the dual-front approach. Barely a month before the IMF talks were confirmed, the Central Bank of Kenya Governor disclosed during the IMF-World Bank Spring Meetings in Washington that the country is also in separate discussions with the World Bank under its Rapid Response Support programme, a fast-disbursing window designed to move liquidity within days during acute shocks. The exact figure was not disclosed, though the Governor described it as "significant."

Two simultaneous borrowing conversations with the world's two largest multilateral lenders is not a sign of financial strength. It is a sign of how thin the buffers have become.

Africa Has Seen This Script Before

Kenya is not alone in this position, and that context matters. Nigeria's total public debt had reached N159.27 trillion, approximately $111 billion, by the end of 2025, a figure driven by oil revenue collapses, naira devaluations, and infrastructure gaps that successive governments preferred to borrow around rather than fix structurally.

Over 80% of Nigeria's government revenue currently goes to debt servicing, according to BudgIT. That is not a debt profile. That is a country mortgaging its operational capacity one tranche at a time.

Zambia went through a formal debt default in 2020 and spent years in restructuring negotiations. Ghana completed an IMF-backed debt restructuring in 2023 after a balance-of-payments crisis that wiped out foreign reserves and sent inflation past 50%.

Ethiopia restructured its external debt under the G20 Common Framework. The pattern across the continent is consistent: borrow to stabilize, reform under conditionality, service the debt, borrow again when the next shock arrives.

What the IMF offers is real, fast liquidity, a credibility signal to markets, and breathing room during a crisis. What it cannot offer is a permanent exit from the underlying vulnerability, which is an economy structurally exposed to external shocks it cannot price, predict, or absorb without reaching for outside money.

Fuel Prices, Politics, and the Arithmetic of Patience

The immediate pressure in Kenya right now is domestic and visceral. Fuel prices have been rising. Kenyans are watching the Energy and Petroleum Regulatory Authority (EPRA) review closely, hoping the government's stabilisation efforts produce something visible at the pump before the next review cycle passes.

This is where macroeconomic abstractions become political facts. Every percentage point of inflation that feeds into transport and food costs is a conversation happening in matatus, markets, and household budgets across the country. Governments that cannot manage that conversation lose the room to manage anything else.

The IMF money, if it comes through, will buy time. Time to stabilise the import bill, reduce pressure on the shilling, and give EPRA something to work with. Whether Kenya uses that time to build a fiscal position that does not require the next emergency programme is the only question that actually matters.

What Kenya Is Actually Signing Up For

The IMF does not send money without a return address. Whatever programme emerges from these negotiations will come with conditions.That is not speculation; it is how every IMF programme in the last three decades has worked.

The 2021 programme in Kenya came with VAT enforcement requirements, energy subsidy reforms, and public wage bill controls. This next one will carry its own list.

The World Bank's Rapid Response Support running parallel to this tells a fuller story. When a government is simultaneously negotiating with two major multilateral lenders at speed, it means the buffers available without external support have effectively run out.

That is the real headline underneath the headline, not that Kenya is borrowing, but that Kenya has reached a point where it cannot absorb a global fuel shock on its own balance sheet.

None of this makes the borrowing wrong, it just makes it more consequential. The conditions Kenya agrees to in the coming weeks will shape its budget, its subsidy structure, and its tax policy for years after the fuel prices stabilize and the Middle East tension fades from the news cycle.

Kenyans watching the EPRA review this week are focused on what petrol will cost in the coming days and the agreement being negotiated right now will determine what everything costs for much longer than that.