Five Money Moves That Are Smarter Than Traditional Budgeting

Traditional budgeting promises control, but real life rarely follows the plan. This article reveals five smarter money moves that work better in an unpredictable economy and explains why the old rules are quietly failing.

Traditional budgeting is the old-school way most of us were taught to handle money.

You sit down, calculate how much you expect to earn for the month, then start sharing it like food in a pot. Rent gets its own portion, transport gets one, food, data, savings, enjoyment, all have fixed slots. You are expected to track every naira and make sure nothing crosses its line.

In theory, it sounds disciplined, however traditional budgeting assumes your income will come as planned, prices will stay reasonable, and emergencies will give you notice.

But fuel can jump overnight, light can disappear for days, and one hospital visit can wipe out an entire month’s plan. Even salary earners know alerts don’t always land on time.

That is why traditional budgeting often feels frustrating here. Once one thing goes wrong, the whole plan scatters. You are not careless, the system just was not built for this kind of unpredictability.

It worked better in a time when money was stable and life moved slower. Today, many Nigerians find that flexibility, backup plans, and multiple income options matter more than strict monthly breakdowns.

Here are five money moves that consistently outperform old-school budgeting, not because they are trendy, but because they are grounded in how money actually behaves in real life.

1. Build Shock Money Before Dream Money

Life does not announce problems ahead of time. One hospital bill, a phone replacement, a delayed alert, or a sudden price increase can wreck a well-planned month.

That is why emergency cash matters more than goal-based savings in the early stages of money management. Its job is simple: protect you from being forced into debt when something goes wrong.

Financial research consistently shows that people with emergency savings are far less likely to rely on high-interest borrowing during crises. This buffer keeps you stable while everything else adjusts.

2. Let Systems Handle the Important Stuff

Money decisions should not require willpower every month. When saving, paying bills, or investing depends on constant attention, mistakes become inevitable.

Automatic transfers and scheduled payments remove emotion from the process. Money moves where it should go without you having to remember or feel motivated.

Behavioural studies show that people who automate their finances save more and default less, even when income is inconsistent. The system works quietly in the background, on good days and bad ones.

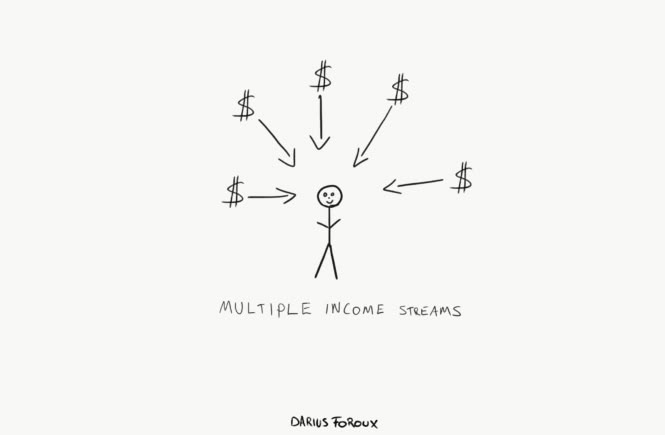

3. Create More Ways Money Can Enter Your Life

Cutting expenses has a ceiling. Income flexibility does not.

Having more than one income source reduces risk. When one stream slows down or disappears, others can carry you through. Economic studies show that people with diversified income recover faster from layoffs and financial shocks.

This does not mean endless hustling. It means building options: freelance work, contract roles, digital skills, consulting, royalties, or equity-based income. The goal is freedom, not exhaustion.

4. Spend Intentionally, Not Equally

Not every expense deserves the same level of attention. Some purchases genuinely improve your life. Others quietly drain it.

Value-based spending focuses on what actually matters to you. You spend freely on those areas and cut aggressively on the rest.

Research in consumer psychology shows that people feel more satisfied with their money when spending aligns with personal values, even if total spending does not change.

Money stops feeling tight when it starts feeling purposeful.

5. Watch Your Direction, Not Just Your Month

Weekly and monthly numbers can be misleading. A bad month does not always mean bad progress.

Net worth shows the real picture. It measures what you own minus what you owe. Tracking it over time reveals whether your financial life is moving forward or standing still.

Why These Moves Work Better

Modern money is unpredictable. Prices change fast. Income is not always stable. Opportunities appear without warning.

What works now is positioning.

Positioning to absorb shocks.

Positioning to take advantage of opportunities.

Positioning to stay calm when things go wrong.

That is the difference between constantly recovering and actually feeling secure.

Discipline is not about tracking every naira. It is about designing systems that work even when you are tired, distracted, or overwhelmed.

When money stops feeling like a daily struggle, it starts behaving like a tool.

And that changes everything.