The Tinubu Economy: If the Charts Look Better, Why Are Nigerians Still Waiting for Relief?

Nigeria’s economy under Tinubu is showing stronger charts in revenue, trade, reserves and growth, but inflation, debt, naira weakness and living costs keep households under pressure.

Ask two Nigerians how the economy is doing and you may get two very different answers.

Ask an economist, and they may point to the charts: foreign reserves are rising, trade numbers are improving, government revenue has grown, and capital inflows are coming back. On paper, Nigeria looks as if it is slowly finding its feet after a rough period.

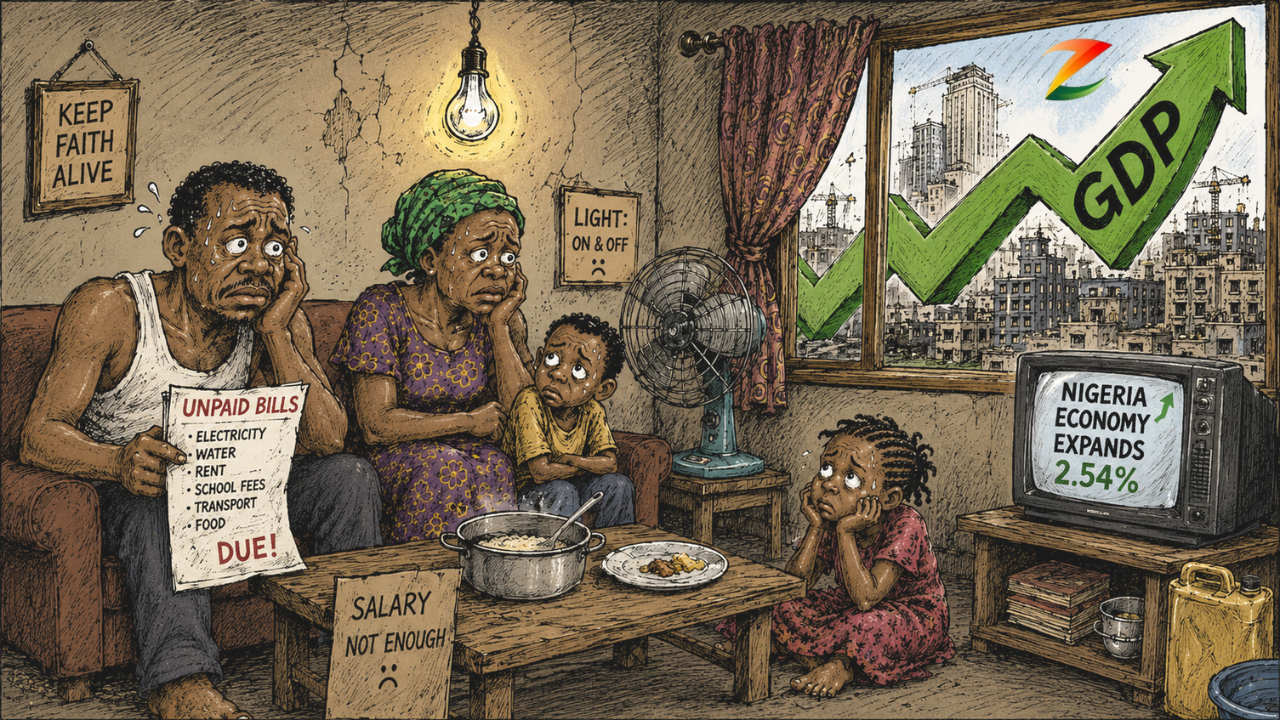

Ask a trader, a salary earner, a parent, or a small business owner, and the answer may sound very different: food is still expensive, transport still bites, rent is harder to pay, and the naira does not buy what it used to.

That is the Tinubu economy in one sentence: better charts, harder lives.

Three years in, the Tinubu economy is no longer just a reform experiment. It is being judged by whether the pain Nigerians were asked to endure is producing visible relief.

So far, the answer depends on where you are looking.

What Tinubu Tried to Fix

Tinubu came into office facing an economy with weak revenue, high inflation, foreign exchange distortions and pressure on public finances. His administration moved quickly with two major reforms:removing fuel subsidies and changing the foreign exchange system.

The promise was that these reforms would reduce wasteful spending, attract investors, improve dollar supply and create a healthier economy over time.

But the administration has rarely answered the harder question: were there less painful paths to the same destination? Economists who broadly support the reforms acknowledge that sequencing mattered.

Some argue that combining subsidy removal and currency floatation simultaneously without adequate social safety nets or wage adjustments already in place, was a choice, not an inevitability. The speed of the double shock left households with no cushion and no transition.

That promise has not disappeared. In fact, some of the numbers suggest the economy is beginning to stabilise. But reforms are not judged only by what they fix on paper. They are judged by what they do to people’s lives while the fixing is taking place.

And that is where the pain has been heavy.

How Reform Entered the Household Budget

The first shock came through fuel. Once subsidy was removed, petrol prices rose sharply. Transport fares followed. Businesses paid more to move goods. Traders passed part of that cost to buyers.

Then came the naira shock. After the foreign exchange reforms, the currency weakened sharply, moving from around N462 to the dollar in April 2023 to more than N1,500 to the dollar by March 2024.

For a country that depends heavily on imported goods and production inputs, that depreciation could not stay inside the financial markets. It entered shops, pharmacies, factories, supermarkets, schools and kitchens.

A food seller who buys ingredients every morning does not need an inflation chart to know margins have collapsed. A parent paying school fees does not need a lecture on exchange rate reform to know the naira has weakened. A commuter understands reform through the fare paid before reaching work.

This is why the debate over Tinubu’s economy feels so personal. The reforms may have targeted structural problems, but their first major impact was on household survival.

Inflation Became the Everyday Headline

Inflation became the clearest face of the crisis. It reportedly climbed to 34.8% in December 2024, while food inflation moved close to 40%.

Those numbers matter because they describe something families already knew: the same money was buying less.

If you are standing in the market, inflation is not an abstract percentage. It is the moment you remove one item from your list because the total has passed your budget.

For many households, adjustment meant smaller food portions, cheaper alternatives, fewer trips, delayed bills and harder choices. For businesses, it meant raising prices, reducing stock, cutting expenses or absorbing losses.

Even when inflation later began to ease, many people did not feel real relief. Lower inflation does not mean prices have returned to where they were. It simply means prices are rising more slowly.

That is why official improvement can still sound strange to people paying market prices.

Why More Government Revenue Has Not Meant More Relief

One of the better charts for the Tinubu administration is revenue. Federal Government earnings rose sharply after the reforms, helped by tax collections, customs receipts, oil earnings and the naira value of dollar-linked income.

But there is a problem: debt servicing has also surged.

Debt service rose from N1.24 trillion in the first quarter of 2023 to N4.86 trillion by the fourth quarter of 2025. A weaker naira made external debt more expensive in local currency, while high interest rates raised borrowing costs at home.

So government may be collecting more, but it is not necessarily freer to spend. When a large share of revenue goes into debt service, less is available for roads, electricity, hospitals, schools, security and support programmes.

For citizens, higher revenue only becomes meaningful when it shows up in better services and lower pressure. That part is still missing.

Who Feels Recovery First?

The first people to feel reform gains are rarely the same people who feel reform pain.

Investors may respond quickly to higher yields and a clearer exchange rate. Exporters may benefit from a weaker naira. Government revenue agencies may collect more. Financial markets may look more attractive.

But salary earners, commuters, import-dependent businesses, low-income households and young people looking for work often wait longer.

They meet reform first through higher prices, not higher income.

This helps explain the gap between market confidence and public frustration. Capital inflows can improve without jobs becoming easier to find. Foreign reserves can rise while families still cut back on food. GDP can grow while wages remain weak.

The economy may be repairing some of its foundations, but many people are still standing outside the building.

Growth Is Not the Same as Comfort

Nigeria’s GDP growth improved from 2.74% in 2023 to 3.38% in 2024 and 3.87% in 2025, supported mainly by services and non-oil sectors.

That growth shows the economy has held up despite the pressure of reform. But growth figures alone do not settle the matter.

For most Nigerians, the economy improves when work becomes easier to find, salaries last longer, businesses can borrow at reasonable rates and prices stop running ahead of income.

Until then, GDP will feel distant.

This is the central challenge of the Tinubu economy. It has impressed parts of the market before convincing many of the people paying the cost.

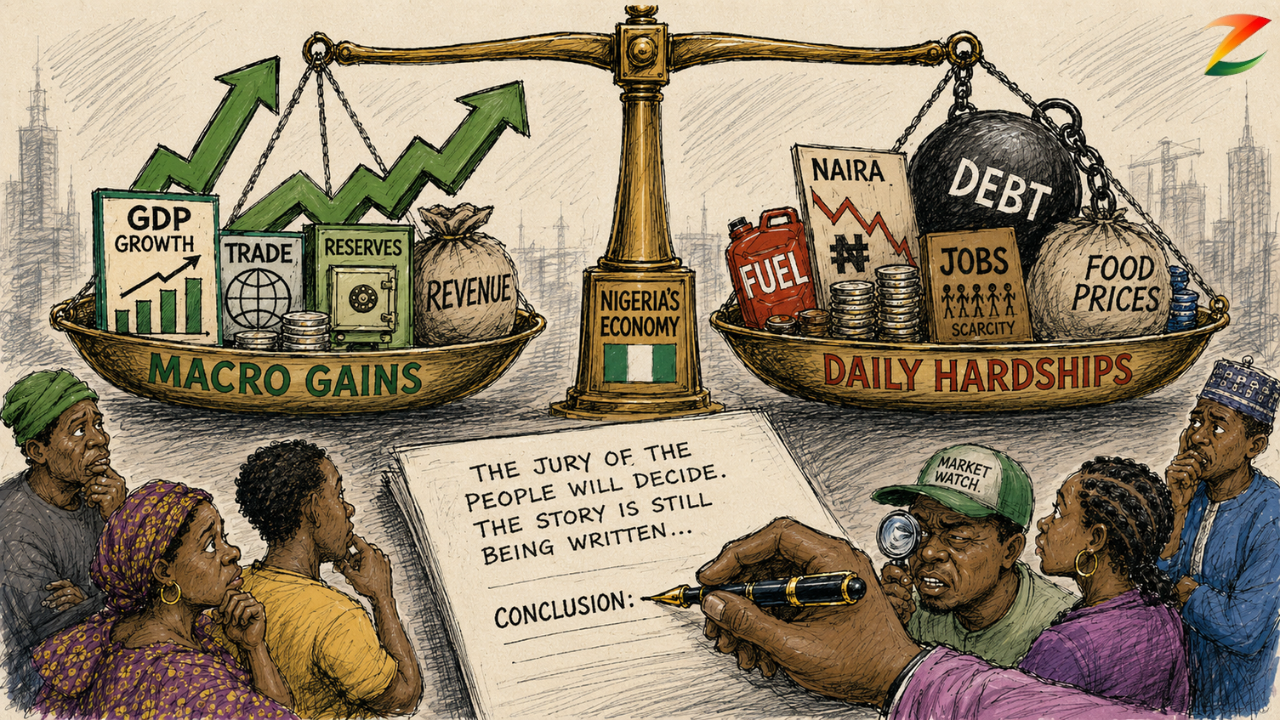

The Verdict Is Still Being Written

The Tinubu economy is not a simple success or failure story. It is an economy in transition, with visible gains and visible wounds.

The charts show stabilisation: stronger reserves, better trade numbers, higher revenue, recovering capital inflows and modest growth.

Daily life shows the unfinished work: expensive food, weak purchasing power, high transport costs, costly credit, heavy debt service and limited job relief.

What the administration cannot afford now is patience as a strategy.

Markets can be won back with data. People require something harder to manufacture: proof, in their daily lives, that the direction of travel is real.

If you are judging the economy from a household budget, the question is not whether the charts have improved. It is whether food is easier to buy, transport is less punishing, businesses can breathe, and salaries last longer.

Until then, the Tinubu economy will remain what many Nigerians already know it to be: better charts, harder lives.