The Headwinds of Innovation: Current Problems Plaguing the Fintech Industry.

The challenges facing the fintech sector ranges from compliance headaches and cybersecurity threats to infrastructure fragility, workforce gaps, and trust deficits. Learn more about these in this article.

For more than a decade, the global fintech industry has been defined by a single narrative: Innovation is fast. Innovation is disruptive. Innovation is the future of finance. But as the sector matures, a more complex narrative is emerging. The very innovations accelerating fintech's growth are also exposing structural weaknesses, regulatory tensions, and new forms of operational risk. An industry once proud of its speed now faces the consequences of scale.

The early days of fintech were characterized by experimentations. Consumer demand was healthy, regulators were lenient, and venture capital flowed freely. The aim was to grow, dominate, and replace legacy processes through digital efficiency. That age is now passing. Investors want to see profitability. Regulators seek control. Users want safety and reliability. And fintech are learning that technological disruption brings its own pressure points.

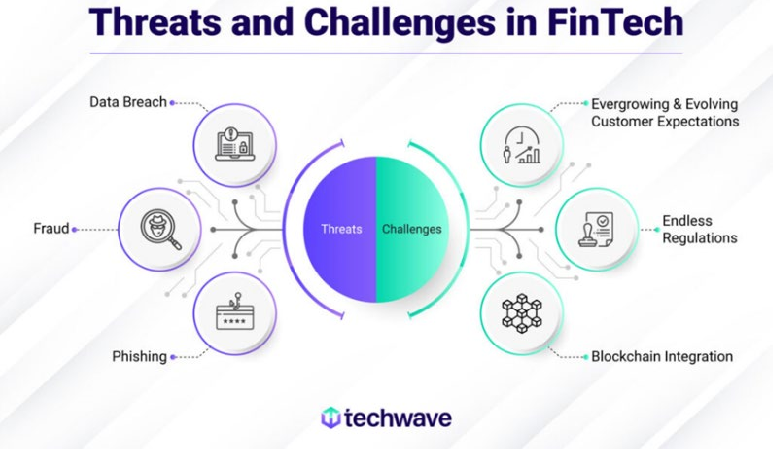

The challenges facing the sector are not small: from compliance headaches and cybersecurity threats to infrastructure fragility, workforce gaps, and trust deficits. The underlying truth is this; the future of fintech rests on stability and resilience.

The Regulatory Tightrope

The more influential fintech become, the heavier the hand of regulators. This, of course, is a delicate balancing act. Regulators seek to balance consumer and financial stability with the desire to support growth. Fintech themselves wish to innovate, free from rules clearly designed for very different types of institutions. What this amounts to is a regulatory landscape that resembles something of a tightrope walking balancing act.

Regulatory Arbitrage: Many fintech operate across multiple jurisdictions; payments companies, neobanks, digital lenders, and cross-border remittance platforms often serve users in regions with conflicting regulatory expectations. Some markets classify them as financial institutions. Others classify them as software providers. This creates uncertainty and exposes companies to unexpected compliance risks.

Regulatory arbitrage occurs when fintech exploit these differences to offer services in ways that legacy banks cannot. But that strategy is fragile. Regulators are coordinating across borders more and more, narrowing the gaps that fintech previously depended on. When the rules suddenly tighten, companies that built their business model on regulatory flexibility struggle to adjust.

AI Governance: AI is at the heart of fintech. It underpins underwriting models, fraud detection, customer support, chatbots, trading algorithms, and risk scoring. However, there is no consistent legal framework for the governance of AI. Regulators don't agree on how machine learning models should be tested, monitored, audited, and disclosed.

This creates three major issues:

Bias and explainability concerns in credit decisions.

Lack of ethics guidelines for using consumer data in training models.

Legal uncertainty over liability when AI-driven financial decisions lead to harm.

The lack of clear-cut rules puts fintech in a precarious position. If they innovate too fast, they run the risk of violating emerging regulations. If they innovate too slow, they lose the competitive edge.

Cybersecurity and Trust Deficits

Trust is essential for fintech innovation. There needs to be trust in a platform's ability to protect user data, secure transactions, and safeguard identity. But the more digital and interconnected fintech becomes, the more exposed it is to cyber threats.

Third-Party Risk: Fintech heavily depend on third-party service providers. There is a need for cloud vendors, API partners, identity verification services, payment processors, data analytics firms, outsourced engineering teams, among others, for daily operations. This means an extended attack surface.

One vulnerability in a cloud partner exposes millions of users. One poorly configured API exposes sensitive financial information. A breach in an identity verification provider can trigger wide scale fraud across multiple platforms. The risk is shared, but the damage is borne by the fintech brand.

AI-Powered Social Engineering: The sophistication of cyber-attacks is on the rise. Attackers use AI to develop hyper-targeted phishing messages, real-time voice impersonation, and convincing fraudulent content. It has become quite difficult for users to differentiate between fake notifications from actual ones.

As AI-driven scams become more believable, consumer trust in digital financial services erodes. This is a particular problem for neobanks and digital-only platforms whose whole model depends on the idea that finance can be safely accessed through devices and apps.

Scaling and Profitability Pressures

The global economic environment has changed. The era of soft money, low interest rates, and unlimited venture funding is over. Fintech should now be able to show sustainable growth, operational discipline, and real revenue. This shift is exposing pressure points that remained hidden during the growth-at-all-costs phase.

Increasing Customer Acquisition Cost: Fintech is crowded. Payments, remittances, digital banking, crypto trading, personal finance apps, and lending platforms all compete for the same users. This drives customer acquisition costs to levels that make long-term profitability challenging.

The competition is not only amongst fintech. Banks have upped their digital capabilities and technology giants have also entered the financial space. This forces fintech to spend more on marketing, incentives, and rewards. The strategy is expensive and rarely sustainable.

Infrastructure Scaling Issues: Fast user growth can expose system architecture weaknesses. When platforms grow more quickly than anticipated, the underlying infrastructure frequently cannot keep up. The consequences include:

Server downtime.

Payment delay.

KYC verification bottlenecks.

Fraud spikes.

Customer support overload.

These operational failures damage trust and can trigger regulatory scrutiny. They also raise costs because the company has to rush to upgrade infrastructure under pressure rather than build it carefully.

The Path To Profitability: The higher interest rates have increased the cost of borrowing for fintech. Investors have grown less patient with long-term burn rates. Many companies today are faced with tough choices:

Decrease expansion into new markets.

Cut staff.

Introduce fees or reduce incentives.

Kill off the unprofitable product lines.

Consider mergers and/or acquisitions.

The transition from growth to sustainability is proving a challenging task.

Talent and Cultural Gaps

Fintech is essentially an intersection of finance and technology, creating a very special challenge. The companies have to hire specialists who understand financial regulation, risk management, compliance, distributed systems, machine learning, cybersecurity, and product design. Such multidisciplinary talents are rare.

Bridging Finance and Tech: There is a shortage of bilingual professionals who understand both languages. There are few engineers who understand banking regulations. There are even fewer compliance experts who understand algorithmic systems. And that naturally creates communication gaps that slow down product development and increase the risk of regulatory missteps.

The Reality of Integrating Legacy Systems: Many times, fintech needs to be integrated with older financial institutions. Banks, insurance companies, and payment processors continue to use legacy systems that are several decades old. These are inflexible systems that are hard to modify. Integration of these with the modern API-based fintech products requires specialized expertise and is a high-investment activity. This makes onboarding slower, delays product launches, and raises the cost of innovation.

Cultural Misalignment: Fintech cultures are often focused on speed and experimentation, while traditional financial institutions are concerned with stability and compliance. When partnerships do take place, the mismatch in decision-making styles can cause tension. These differences become obstacles to stall innovation.

The Trust and Stability Question

Beyond these structural issues, there is a larger challenge before fintech. Users are getting increasingly sensitive to risk. Economic downturns, data breaches, bank collapses, and digital scams have made consumers cautious.

Fintech can no longer rely on novelty. They need to prove reliability: that digital platforms can be as safe and stable as any traditional institution. Meeting these shifting expectations will demand improved security frameworks, increased transparency, clearer communication, and deeper regulatory cooperation.

Trust is what will make or break the future of Fintech.

Where Innovation Meets Reality

The fintech industry has arrived at an inflection point. Its early successes created an impression that technology could solve every financial problem. But the deeper the industry grows, the clearer its vulnerabilities become.

The headwinds facing fintech are not temporary. They reflect a fundamental shift in the industry's lifecycle. The sector is moving from rapid experimentation to structural maturity.

Success now will depend on resilience, compliance, infrastructure strength, and operational discipline. Innovation will continue, but it will be scrutinized more closely.

Growth will continue, however, it must be sustainable. Those companies that survive will be the ones embracing the complexity of modern finance rather than seeking to bypass it. The biggest challenge for Fintech today is now about building strong.