Nigeria Exits FATF Grey List: Economic Boost and Global Trust Restored

Nigeria has been officially delisted from the Financial Action Task Force (FATF) grey list, a significant development announced on October 24, 2025. This decision marks a pivotal moment for the West African nation, signaling enhanced global confidence in its financial system and affirming its commitment to robust anti-money laundering (AML) and counter-terrorism financing (CFT) frameworks. The delisting comes after two years of intensive reforms and coordinated efforts by various national institutions.

The FATF had initially placed Nigeria on its grey list in February 2023, identifying it as a "jurisdiction under increased monitoring" due to serious gaps in its regulatory and compliance systems regarding illicit financial flows, money laundering, and terrorist financing. This designation led to immediate and far-reaching consequences. International banks and investors became highly cautious, subjecting Nigerian transactions to stricter scrutiny and higher compliance costs. The country experienced a slowdown in foreign direct investment (FDI), weakened correspondent banking relationships, and a damaged reputation within the global financial system. There were even reports of some merchants in Europe and the United States rejecting electronic transactions from Nigerian cards, exacerbating issues already present due to foreign exchange challenges.

The turnaround is attributed to deliberate and coordinated policy actions led by the Nigerian Financial Intelligence Unit (NFIU), the Central Bank of Nigeria (CBN), the Minister of Justice/Attorney General of the Federation, and the Economic and Financial Crimes Commission (EFCC), all operating under a reform-driven administration. A major shift in confidence occurred with the assumption of office by Central Bank Governor Olayemi Cardoso in September 2023. Cardoso emphasized integrity and compliance as cornerstones of financial reform, tightening oversight, enforcing stricter AML and CFT standards, and ensuring accountability for non-compliant banks. According to Cardoso, the delisting reflects a clear policy direction and the coordinated efforts that have delivered sustainable, standards-based reforms, reinforcing the integrity of Nigeria's financial system.

The removal from the grey list is widely celebrated by financial experts and business leaders. Olugbenga Agboola, co-founder and CEO of Flutterwave, hailed it as a "massive win" for the Nigerian economy, expecting it to restore confidence, lower remittance and cross-border costs, and unlock faster, cheaper payments. Tayo Oviosu, founder and CEO of Paga, echoed this sentiment, highlighting that it "opens up the country for FDI and engagement from the West." President Bola Tinubu also stated that the delisting marks a new chapter in Nigeria's financial reform agenda.

This development brings a multitude of economic benefits. For individual Nigerians, it is anticipated that transactions will attract less scrutiny, and Nigerian debit cards will gain wider acceptance internationally, potentially reducing rigorous checks at foreign airports. Economically, Ayokunle Olubunmi of Agusto & Co expects the delisting to further stimulate foreign portfolio investment and potentially accelerate Nigeria's inclusion in the Morgan Stanley Index, supporting external reserves and the exchange rate. Economist Abuede Charles added that it positions Nigeria more favorably on the global investment radar, expecting renewed FDI inflows and a boost to the country's sovereign rating, strengthening investor confidence.

The delisting also provides a significant tailwind for President Tinubu's tough monetary reforms, including foreign exchange rate unification. It reassures international investors and domestic stakeholders of Nigeria's transparent, less risky, and globally compliant financial environment, encouraging foreign exchange inflows, improving liquidity, and supporting naira stabilization. For the fast-growing fintech and digital finance ecosystem, exiting the grey list strengthens Nigeria’s standing in cross-border transactions and international payment negotiations, making it easier for fintech firms to attract venture capital and forge global partnerships.

Beyond financial implications, the reforms leading to delisting have fostered deep institutional collaboration across regulators, law enforcement, and policymakers, resulting in improved corporate transparency, beneficial ownership disclosure, and inter-agency coordination. These achievements align with President Tinubu’s anti-corruption and fiscal integrity agenda, reinforcing Nigeria’s reputation as a credible partner in combating illicit financial flows and asset recovery. Nigeria joins other African nations like South Africa, Mozambique, and Burkina Faso in achieving this milestone. The immediate economic effects will likely include lower transaction costs, faster remittance flows, and greater export competitiveness. The challenge now is to consolidate these gains through consistent enforcement, continued transparency, and disciplined reform to ensure Nigeria's return to global financial respectability is permanent.

You may also like...

The 1896 Adwa War: How Ethiopia Defied Colonialism

Ethiopia with the exception of Liberia which was used as a settler place for freed slaves remains the only African Count...

Why We Need Sleep: Inside the Brain’s Night Shift

Even when you’re asleep, your brain is quietly up to something, sorting, cleaning, and working behind the scenes.

When Nollywood Meets Netflix: The Creative Tug Between Local Storytelling and Global Algorithms

Nollywood’s partnership with Netflix is rewriting the script for African cinema, offering global reach but raising quest...

Mozambique's LNG Megaproject: A Promise or Peril?

TotalEnergies is leading a consortium in Mozambique as it promises potential restructuring of the nation's energy se...

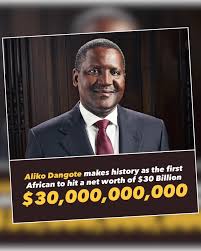

Aliko Dangote, Africa’s Wealth King: First African-Born Billionaire to Cross $30B

Aliko Dangote, the richest Black man in the world, has reached a new milestone, with a net worth of $30.3 billion, accor...

WAEC Conducts Trial Essay Test Ahead of Full Computer-Based WASSCE in 2026

The trial Computer-Based Test (CBT) for the WAEC essay was held on Thursday, October 23, 2025. The exercise was conducte...

Can Long- Distance Love really work?

Can love really survive when touch becomes a memory and connection lives behind a screen? For many, distance isn’t the ...

Nigeria’s Rental Crisis: House of Representatives Moves to Cap Rent Hikes at 20%

Nigeria's rental market has been under intense pressure, and now lawmakers are stepping in. The House of Rep. has called...