Beyond the Hype: Is African Fintech Truly Financial Inclusion or a New Digital Divide?

African fintech is booming, promising inclusion. But is it creating a new digital divide, leaving millions behind? Unpack the hidden truths.

African fintech is a global success story, celebrated for bringing financial services to millions previouslyexcluded by traditional banks.

SOURCE: Google

Yet, beneath the headlines of booming investments and unicorn startups, a critical question emerges: Is this digital revolution truly fostering deep financial inclusion, or is it inadvertently creating a new digital divide, leaving significant segments of the population – particularly the rural poor, the elderly, or those without smartphone access – further behind?

This article will delve into the nuances of fintech's impact, examining how its reliance on digital literacy, smartphone penetration, and stable network infrastructure can exclude as much as it includes.

The Left Behind: Demographics and Regions in the Digital Wake

Despite the widespread acclaim for African fintech, specific demographics and regions within the continent are indeed being left behind by the rapid advancement of mobile money, digital lending, and other fintech innovations. This creates a concerning digital divide driven by access and literacy barriers.

SOURCE: Google

Rural populations are a primary group facing exclusion. While mobile money agents have expanded reach, vast swathes of rural Africa still lack reliable internet connectivity and adequate mobile network infrastructure, which are foundational for consistent use of digital financial services. Even where a basic network exists, it can be unstable or too expensive for daily use.

A 2022 Central Bank of Nigeria report found that 81% of financially excluded Nigerians live in rural areas, highlighting a significant geographical disparity despite overall phone access.

The elderly often struggle with digital literacy and the complexity of smartphone-based financial applications. Many older individuals may not own smartphones, preferring basic feature phones, and even with those, the user interfaces can be unintuitive.

Barriers include a lack of information and understanding, security concerns, language barriers within apps, and a general resistance to change.

Research indicates that many elderly individuals perceive mobile banking as an innovation for young people, facing challenges like vision impairment and difficulty remembering complex login credentials.

This technological gap can deepen their financial exclusion, as bank branches decline.

Women, particularly those in rural areas or with lower literacy levels, also face disproportionate exclusion, though fintech has shown some promise in bridging gender gaps in certain contexts.

While mobile money has helped many women gain financial autonomy by offering privacy in transactions, service providers often deploy "one-size-fits-all" or gender-neutral products that may not adequately address the specific needs or challenges faced by women, such as lower digital literacy rates or limited access to phone ownership.

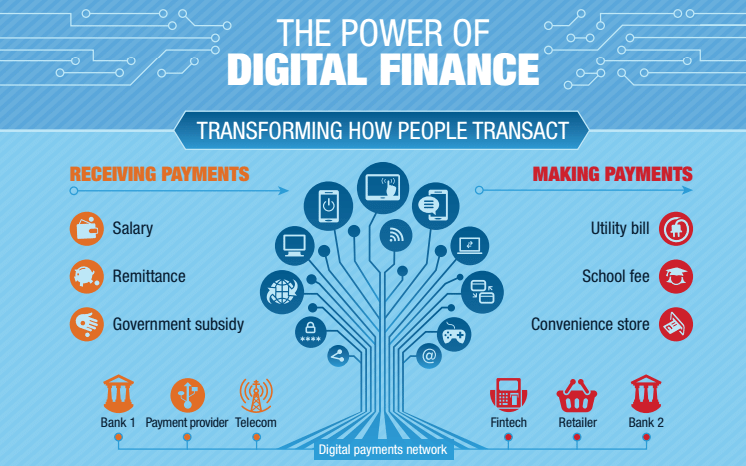

Finally, individuals who rely solely on feature phones (non-smartphones) are often limited in the range and sophistication of fintech services they can access.

While USSD (Unstructured Supplementary Service Data) codes allow for basic mobile money transactions on feature phones, more advanced services like digital lending apps, investment platforms, or complex payment solutions often require smartphone capabilities and internet access.

The digital revolution is largely smartphone-centric, inherently creating a tier of exclusion for those without such devices, who are often among the poorest segments of the population.

Fintech's Shadow: Impact on Informal Financial Systems

The rise of fintech is having a complex impact on traditional informal financial systems in Africa, such as rotating savings and credit associations (ROSCAs like "Susu" or "Chama") and community-based savings groups. While some see synergy, there are concerns about the displacement of vital community structures.

SOURCE: Google

Historically, these informal systems have been the backbone of financial inclusion for millions of Africans, providing access to credit, savings, and insurance without formal requirements like collateral or identity documents.

They are built on trust, social capital, and local knowledge, offering flexible, community-driven solutions that formal banks often cannot. Members often leverage these groups not just for financial transactions but also for social support, collective bargaining, and sharing economic opportunities.

Fintech's emergence presents both competition and potential collaboration. On one hand, mobile money offers unprecedented convenience and reach, sometimes at lower transaction costs than informal alternatives, especially for remittances.

This can draw users away from traditional informal methods, particularly for basic transactions. Some informal lenders (money lenders) may find their market shrinking as digital lending offers faster, albeit sometimes predatory, alternatives.

The convenience and speed of digital solutions challenge traditional systems to adapt or risk obsolescence.

However, the relationship is not purely adversarial. Many informal groups are integrating mobile money into their operations. Instead of physical cash collections, members might send contributions via mobile money, improving security and efficiency.

Some fintech companies are exploring partnerships with these groups, leveraging their existing trust networks and local knowledge to reach underserved populations.

For instance, digital platforms can enable formal savings mechanisms that mirror ROSCAs, or facilitate loan disbursements to group members.

Yet, there's a risk that as formal digital solutions replace informal ones, the crucial social fabric and collective support mechanisms inherent in traditional systems could erode, potentially leaving communities more financially isolated and vulnerable if the digital alternatives aren't equally robust in fostering community resilience.

Concerns also arise regarding the data collected by fintech companies. While this data can inform credit scoring, it also shifts power dynamics away from community-based trust to algorithmic assessments, which might not fully understand local nuances or be accessible for redress.

Beyond the Screen: Solutions for True Inclusion

To ensure that fintech truly achieves widespread financial inclusion rather than creating a two-tiered digital economy, innovative, low-tech, or community-centric approaches are desperately needed. This requires a shift from solely tech-driven expansion to human-centered design and policy.

One crucial approach is agent-assisted models that bridge the digital and physical divide. While mobile money relies on agents, further empowering and training these agents to act as digital literacy educators, customer support, and trusted intermediaries can significantly help bridge gaps for the digitally illiterate or elderly. These agents can guide users through app interfaces, explain security features, and facilitate transactions, bringing the human touch back to digital finance. Expanding agent networks into remote rural areas, supported by robust logistics, is vital.

Secondly, developing simplified interfaces and voice-based technologies can make fintech more accessible to diverse populations.

Designing apps with highly intuitive, minimalist designs, or even voice-activated commands (especially in local languages), can lower the barrier for those with limited literacy or smartphone familiarity.

The focus should be on practical utility over feature richness. Platforms that leverage basic feature phone capabilities (USSD) for more than just basic transfers, perhaps offering micro-insurance or micro-savings products via simple menu navigation, can reach a much wider audience.

Thirdly, integrating and formalizing informal financial systems rather than replacing them offers immense potential.

Fintech providers can partner directly with ROSCAs and savings groups, offering them digital tools to manage their collective funds, track contributions, and disburse loans, thereby enhancing their efficiency and security without dismantling their inherent social value.

This "fintech for groups" approach leverages existing trust networks. For instance, some startups are building platforms specifically for these groups, demonstrating a community-centric approach to digital finance.

Finally, supportive regulatory frameworks and public-private partnerships are essential. Governments must create regulations that balance innovation with consumer protection, ensuring transparency in digital lending and addressing data privacy concerns.

Policymakers should also invest in affordable public internet infrastructure, especially in rural areas, and incentivize fintech companies to develop products tailored for underserved segments. Collaborations between fintechs, traditional banks, local community leaders, and NGOs can drive financial literacy campaigns that address specific cultural contexts and needs.