Banks, Fintechs Disagree on Resuming International Naira Card Use

Since Nigerians now have more options than they did three years ago, the banks have now carved a niche to compete with financial technology (fintech) companies that offer virtual dollar cards as a result of the reintroduction of international transactions on naira cards.

Fintechs like Chipper Cash, GoMoney, Cardtonic, Wallet Africa, BoldSwitch, Geegpay, and Fundall emerged to fill the void left by the announcement by Standard Chartered Bank, First Bank of Nigeria (FBN), Guaranty Trust Bank (GTBank), and Zenith Bank that their Naira debit cards would no longer be able to conduct international transactions between July 2022 and January 2023.

Nigerians without bank dollar cards may now pay for services like Amazon, AliExpress, Netflix, Spotify, YouTube, and other overseas transactions thanks to fintechs.

The fact that banks’ Naira cards can now be used for point-of-sale (POS) payments outside of Nigeria, purchases on foreign websites, and cash withdrawals from automated teller machines (ATMs) overseas is expected to reduce their market share.

With more options opened to Nigerians now and factors that will affect Nigerians deciding the next move, some users told TheCable that their next course of action will depend on a number of factors, including their spending limit, foreign exchange (FX) prices, and the platform’s wider acceptance.

Geoffrey Nwankpa, a regular user of dollar virtual cards, stated that he is open to switching to a bank naira card because of the fees associated with using fintech virtual cards. However, he stated that his decision will be based on the card’s spending limits and restrictions.

Nwankpa also expressed his hope that “the commercial banks would not put absurd limits on international transactions,” even if he acknowledged that paying for transactions abroad would no longer be challenging. If he considers setting a $1,000 monthly cap for himself for foreign payment and subscriptions. It won’t work. He thus hopes that their boundaries will be reasonable.

He further added that since one of the fintechs he uses charges outrageous and exorbitant rates, currency rates should also be taken into account.

“You could buy a dollar for N1,800, and then sell it for about N1,500. You also have to pay $1 a month for card maintenance. There will be a deduction if you transmit or receive USDT,” he stated.

He also made a clear example: if he were to consider sending $100 out of my fintech wallet, approximately $98.5 would be my exchange. The same is true for receiving.

Furthermore, another user by name Odudu Inyang-Udoh, who uses two virtual credit cards, claimed they are “seamless,” but he is unsure if he will stick with fintech platforms due to personal reasons which were not shared.

Inyang-Udoh stated that “transaction charges and limits, exchange rates, etc.” will determine his choice, although he would be happy to move if the naira debit card provided better value for money while making purchases online.

Reliability is important to him in terms of broader platform acceptance, he continued.

The ease of paying for online and web based transactions, particularly on global platforms, is another potential benefit. However, everything relies on how much the benefits of utilizing a naira debit card outweigh those of virtual credit cards, according to Inyang-Udoh.

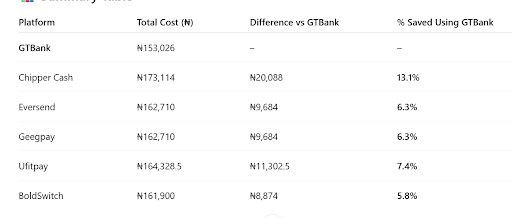

An anonymous user finally shared that FINTECHS won’t harass him with FX fees the way they used to. He also shared how he can be able to save using GTBank with other fintechs for online and web payment and transactions.

With the difference between a virtual and a naira card for overseas transactions Wema Bank and First Bank offers $1,500 quarterly, GTBank limits customers to $1,000 quarterly, and UBA has a $1,000 daily and monthly restriction depending on the card used TheCable is aware that banks have lower transaction limitations than fintechs.

Fundall has no limit, however Chipper Cash and Eversend have a $10,000 monthly spend cap, Geegpay limits users to $5000, and Ufitpay has a $2,000 monthly limit.

Additionally, the maximum transaction amount for Sendbit and BoldSwitch is $10,000.

As of July 11, the official and parallel currency rates are N1,530.26 and N1,550/$, respectively. However, the FX prices for Chipper Cash and Eversend are N1,714/$ and N1,619, respectively, according to Monierate.

While Boldswitch provides charge-free transactions on US websites, transactions involving other currencies incur 2.5 percent of the transaction value. On charges, virtual card operators such as Geegpay withhold $0.5 for dollar transactions and 0.9 percent of the transaction value for non-dollar purchases.

Additionally, Eversend levies a 3.5 percent fee when users pay with euros and pounds, even though it charges a $0.50 fee per transaction.

Additionally, Ufitpay charges 1.5% for every USD virtual card transaction.

However, value-added tax (VAT) is the only tax that banks like GTBank and UBA deduct from each transaction.

TheCable was also informed by one of the fintech firms ‘BoldSwitch’ that its business operations will not be impacted by the resumption of foreign and international transactions on the naira card.

According to BoldSwitch, “many users continue to look for alternative platforms that offer higher transaction limits, faster access, and more flexible onboarding than traditional banks, so our value proposition remains intact.”

“It is a positive thing that consumers may have additional options now that the suspension has been lifted. However, stringent monthly restrictions, high rejection rates on international platforms, and unstable foreign exchange rates are common features of bank-issued naira cards.

“Boldswitch still provides access to international payments, stability, and transparency without the regular headaches. There is hope to see more interest in the field, but not necessarily a drop in the need for our services.

Boldswitch stated that it has developed a number of infrastructures to improve user experience, including AI-powered features catered to users’ requirements, as part of its strategy to keep consumers in the face of increasing competition from commercial banks.

Additionally, we are creating more business-oriented options for creator and in-store payments that banks do not already offer. Essentially, we’re creating a cutting-edge digital finance ecosystem tailored to the needs of young Africans and the diaspora, not merely offering financial services,” the company stated.

Additionally, Cardtonic, a digital exchange platform, stated that it is a good thing since Nigerians should not be prevented from spending money abroad “just because they are Nigerians.”

However, the business stated that it continues to weigh the present situation.

Ayokunle Olubunmi, head of financial institutions ratings at Agusto & Co., commented on the issue, in relation to the impact and the little restrictions stating that most customers shifted to using the lenders’ dollar cards after banks stopped naira transactions on dollar cards.

As a result, Olubunmi pointed out that the effect on fintechs might be minimal because of how small their customer base is now.

The banks that recently removed the ban on dollar transactions using naira debit cards “still had a limit,” he added.

According to Olubunmi, the present authorized expenditure is still somewhat limiting, in contrast to earlier times when service users had a very high limit and could conduct a variety of transactions.

He remarked, “It is not nearly where we used to be, but it is better than zero.”

“Even though some fintechs may experience a drop in transactions, consumers may still choose to use them.”

“If one area is not working, they can pivot into something else,” Olubunmi continued, referring to the business strategy of fintechs.

Olubunmi went on to say that banks and fintechs can work together in more areas than they can compete.

Due to a lack of money, particularly for domiciliary accounts, fintechs are unable to effectively compete with banks. According to him, they don’t have as much of it as the banks have.

“The majority of fintech companies either change their focus or figure out how to work with banks.”

Charles Abuede, a research analyst at Cowry Asset Management Limited, provided remarks, stating that the recent move indicates more trust in the foreign exchange market and better liquidity in the banking system.

Abuede went on to say that the change in policy might possibly be a calculated move to increase foreign exchange inflows, particularly from remittances, by increasing system trust and facilitating international payments.

Subscribe to get the latest posts sent to your email.

You may also like...

Diddy's Legal Troubles & Racketeering Trial

Music mogul Sean 'Diddy' Combs was acquitted of sex trafficking and racketeering charges but convicted on transportation...

Thomas Partey Faces Rape & Sexual Assault Charges

Former Arsenal midfielder Thomas Partey has been formally charged with multiple counts of rape and sexual assault by UK ...

Nigeria Universities Changes Admission Policies

JAMB has clarified its admission policies, rectifying a student's status, reiterating the necessity of its Central Admis...

Ghana's Economic Reforms & Gold Sector Initiatives

Ghana is undertaking a comprehensive economic overhaul with President John Dramani Mahama's 24-Hour Economy and Accelera...

WAFCON 2024 African Women's Football Tournament

The 2024 Women's Africa Cup of Nations opened with thrilling matches, seeing Nigeria's Super Falcons secure a dominant 3...

Emergence & Dynamics of Nigeria's ADC Coalition

A new opposition coalition, led by the African Democratic Congress (ADC), is emerging to challenge President Bola Ahmed ...

Demise of Olubadan of Ibadanland

Oba Owolabi Olakulehin, the 43rd Olubadan of Ibadanland, has died at 90, concluding a life of distinguished service in t...

Death of Nigerian Goalkeeping Legend Peter Rufai

Nigerian football mourns the death of legendary Super Eagles goalkeeper Peter Rufai, who passed away at 61. Known as 'Do...