With how fast-moving and intertwined markets have become this year, it's become next-to-impossible to cut through the noise.

It's hard enough trying to keep your fingertip on the pulse at all, let alone find the time to apply it all through a localised lens.

Thankfully, the experts have us covered.

On the second day of Morgan Stanley's Australia Summit, Chris Nicol, head of macro strategy for Morgan Stanley Australia, spoke to Alexandre Ventelon, Head of Investment Strategy for Morgan Stanley’s Wealth Management division, on the current state of play locally.

.jpg)

Only 1% of Australia’s GDP is exposed to tariffs, and there aren’t many first-order impacts on Australia from the trade war.

Of course, there are some second-order impacts to be wary of - a potential slowdown in the Chinese economy, AUKUS and the wider friction created during a global trade war.

There’s also the worry that the disinflationary effect of tariffs will not be as pronounced as many expect.

Some are predicting Australia to have the strongest growth of any country in the G20.

But while we remain very resilient as an economy, we had “anaemic” growth in the second half of 2024, says Nicol.

He predicts growth will come in below the 2% being forecast elsewhere, especially as almost all of our recent growth came from government spending, including two-thirds of jobs growth.

He also expects the newly-reelected Labor government to pay for growth through taxation, not spending cuts.

“What's going to be interesting is how they pay for that.”

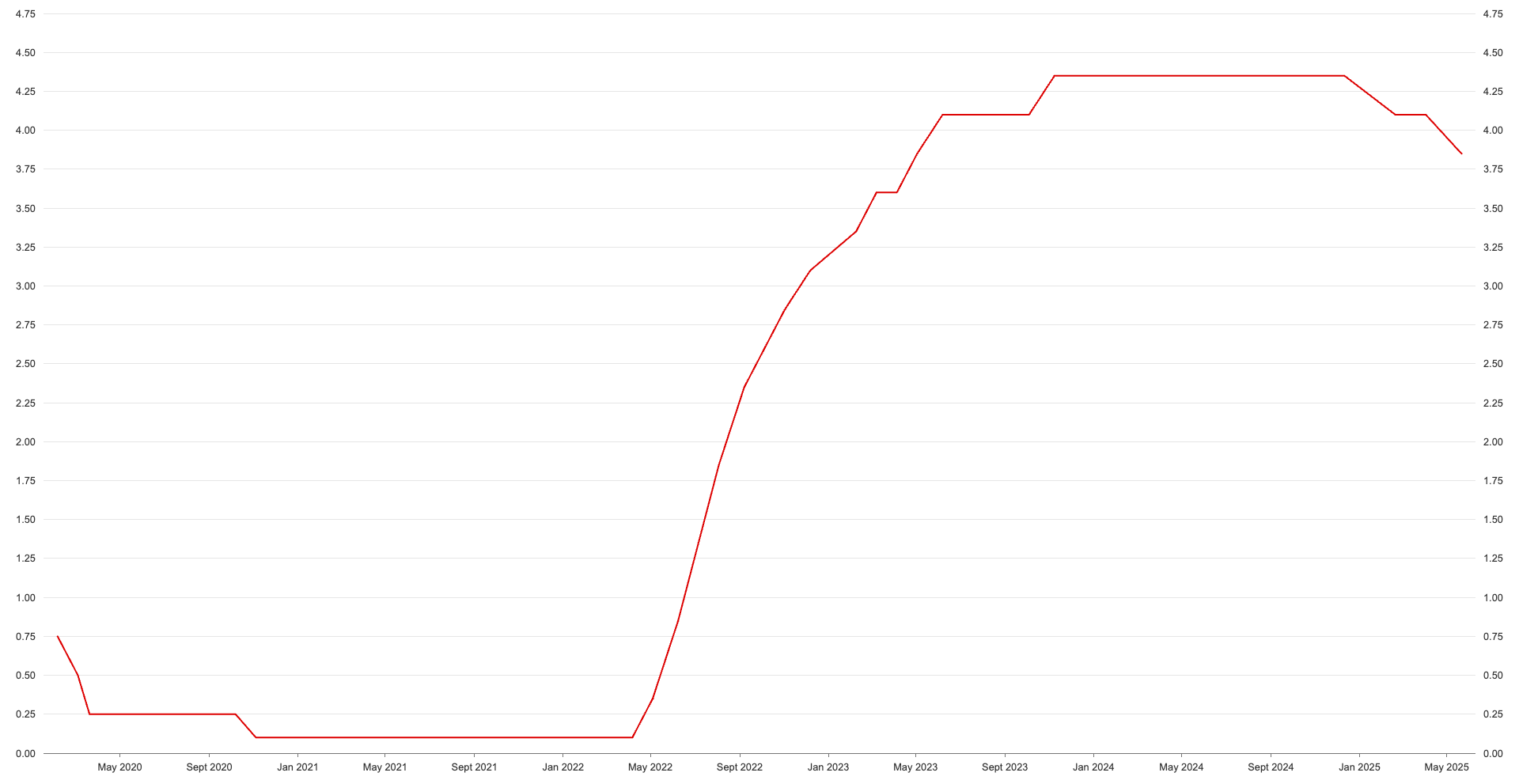

The Morgan Stanley team is one of the few to boast a perfect record on predicting recent RBA rate changes, but even they were surprised by the RBA’s dovish pivot.

Nicol says they expect the cash rate to settle into a neutral position, perhaps getting as low as 2.7%, but maintain a terminal rate of 3.1%.

Global uncertainty means the RBA doesn't want to be too restrictive, argues Nicol, which translates to two more cuts this year and one next year.

By way of comparison, Morgan Stanley sees no cuts from the Fed this year, but seven in 2026.

On the stock market side, Nicol is also fairly positive.

“Investors have been asking the question: is Australia truly defensive?”

Offshore flows and the recent bounce have proved it is, believes Nicol. The ASX has become “not just a nice place to visit but to stay a while” for investors.

Despite the ASX 200 already being above Morgan Stanley’s 12-month target, Nicol believes the market is fairly valued, and suggests there could be some cyclical action around interest rates, housing and earnings growth.

“Earnings is where rubber hits the road,” says Nicol.

Of course, there is a risk of stagnation if government spending dries up given the weak spending coming from the private sector.

The Aussie banks have dually-benefitted from the move to defensives and the move to domestic-focused companies, but are in effect trading like highly-leveraged utilities.

They’re just “one big mortgage”, in Nicols words.

The Commonwealth Bank (ASX: CBA) price surge can also be put down to a couple of factors, he says.

There’s a lot of long-term holders who aren’t selling, which puts the free float for CBA closer to $40 billion in his estimation, against a $300 billion market cap.

There’s also a lot of price-agnostic buyers, mostly in the form of passive investing flows from overseas.

CBA is the 10th largest stock in the ex-USA Global MSCI index, which means it will continue to get bought up disproportionately to even the rest of the Big Four.

The bond market has become a hard place to invest, especially long-term bonds, because of the prevailing uncertainty.

“We should be buying 30-year US Treasuries” says Nicol, but the current environment makes that a challenging play because of the possibility that yields may go higher.

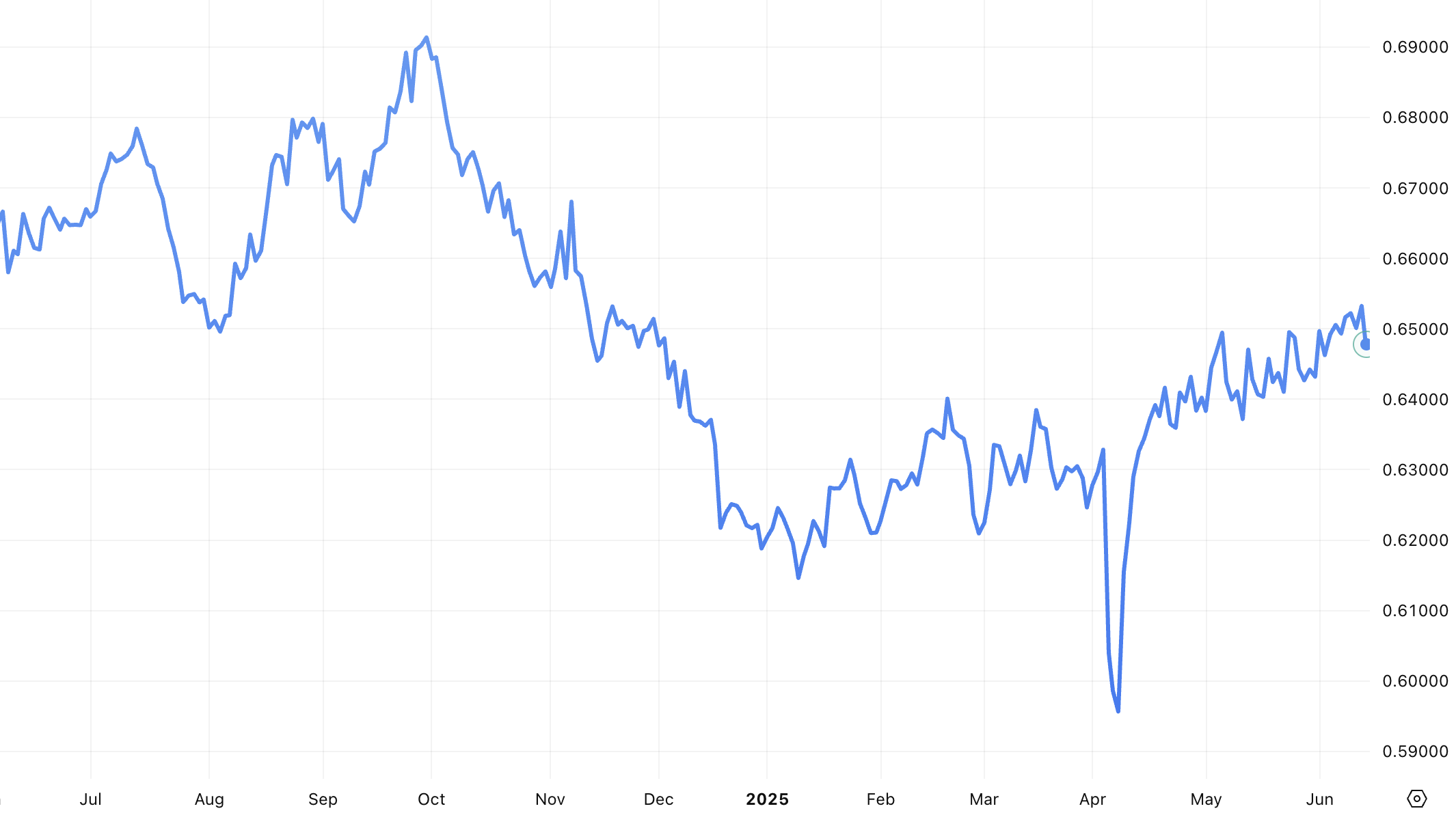

He also expects AUD to continue its recovery against the US dollar, and sees US$0.70 as fairer value, but doesn’t expect it to rise against the euro.

“Every strategist has to have gold in their portfolio,” said Nicol. “Gold itself can hold these levels and has a bull case for higher levels.”

He says every fund manager has one or two gold stocks in the top 100, but in the small and mid cap space that number is higher, meaning those managers have to be exposed to gold.

Information is everywhere; true insight is rare. Morgan Stanley brings knowledge and experience from across the globe to make sense of the issues that matter. Find more insights here.