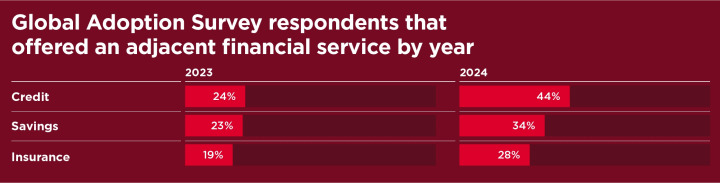

In 2024, more mobile money providers, or MMPs, were offering access to credit, savings, and insurance products than the year before. These figures show an ongoing trend where MMPs are going beyond their typical payments use cases by offering what’s known as “adjacent services.”

For providers, this is part of a drive to maintain customer stickiness and ensure commercial viability. For users, some of these products have helped to improve their ability to deal with unforeseen events and shocks, such as natural disasters or climate events.

Credit is now considered the use case that many providers are keen to grow. When thinking beyond payments, credit is considered a natural next step — not just short-term and unsecured microloans, but lending over the medium term to enable more productive outcomes. As of June 2024, nearly 45% of the MMPs we surveyed offered credit. As a result, we found that the number of customers who took out loans through mobile money grew by 50% between September 2023 and June 2024.

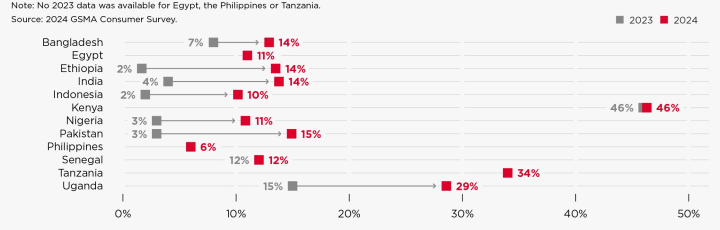

For the first time, GSMA noted this trend across selected markets based on consumer data collected in 12 markets in Africa and Asia: Bangladesh, Egypt, Ethiopia, India, Indonesia, Kenya, Nigeria, Pakistan, the Philippines, Senegal, Tanzania, and Uganda. Our analysis showed that a rising number of customers in Asia and sub-Saharan Africa had used mobile money to take out a loan in 2024, compared to 2023. In markets such as Ethiopia, India, Pakistan, and Uganda, this year-on-year increase was over 10 percentage points.

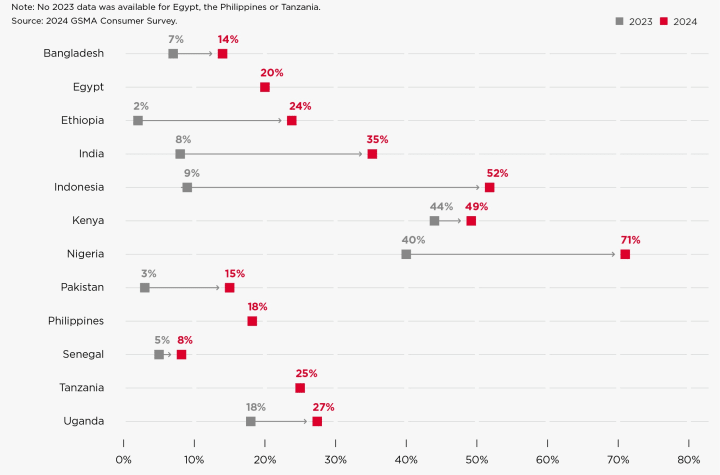

In 2024, like in previous years, savings offerings were the second fastest-growing noncore products — 34% of MMPs offered savings, an increase from 23% in 2023. Similar to the trend on credit, the increase in available savings products has led to an 80% increase in customers saving money between September 2023 and June 2024. Crucially, where MMPs collected this data, 91% of providers saw an increase in the cumulative number of unique female customers saving via mobile money accounts.

Interestingly, savings is not significantly affected by a lack of interest payments — though this remains a powerful incentive. Saved funds are often split between customers using a dedicated interest-bearing savings subwallet within mobile money accounts (in markets where regulations allow interest to be paid on mobile money balances) while others simply use mobile money as a reliable store of value. We observed the latter in parts of sub-Saharan Africa, such as Botswana, where mobile money providers can offer convenient financial services to remote customers.

Around 50% of the mobile money providers surveyed by GSMA in 2024 offered either a credit, savings, or insurance product.

—

The World Bank Group’s Global Findex Database 2021 found that 5% of adults in low- and middle-income countries saved using a mobile money account. In sub-Saharan Africa, 15% of adults — or 39% of all mobile money account owners — saved using a mobile money account. Our consumer survey in 2024 found that the number of customers using mobile money for savings over the past 12 months grew by more than 20 percentage points in Ethiopia, India, Indonesia, and Nigeria.

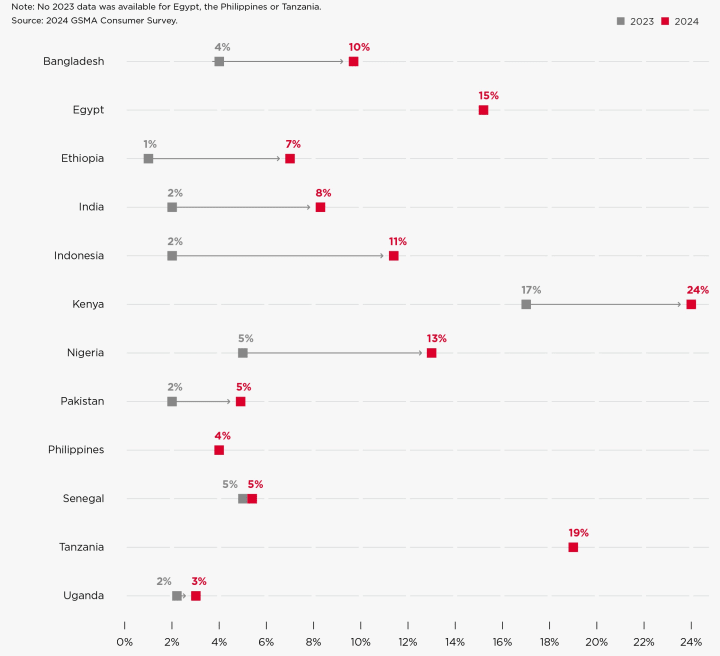

Among the three adjacent services, insurance is the least offered. Under a third of mobile money providers offered insurance in 2024, though this marks a significant improvement from the prior year, when only 19% of MMPs offered insurance. This growth is part of an effort among several MMPs to position themselves as a lifestyle platform for customers — and offering a range of financial services is key to this strategy.

Of the MMPs that provide access to insurance services, 85% offer life or funeral cover and health insurance, known as hospital cash insurance. While MMPs can play a range of roles in an insurance value chain, most are relied on as payment channels for premiums and claims. Some mobile network operators and MMPs, notably Safaricom in Kenya and MVola in Madagascar, have acquired insurance broker licenses to play a bigger role in creating and distributing insurance products to offer their customers crucial shock protection.

When looking at demand-side figures from our 2023 and 2024 consumer surveys, the percentage of customers using mobile money to pay for insurance increased in nearly all countries that supplied data across both years. Some markets saw significant year-on-year growth, including Bangladesh, Ethiopia, India, Indonesia, Kenya, and Nigeria.

As adjacent services become core value propositions for MMPs, there is a sense that these products can drive financial health. This will not be without challenges: In some markets, such as East Africa, digital credit is seen to be contributing to overindebtedness. Conversely, in other markets, GSMA found that digital borrowers may feel financially healthier because digital loans enable quicker access to additional cash for expenses. These customers can also grow their savings as they use loans for both routine and unexpected costs.

For mobile money providers, expanding use cases is necessary to remain relevant as consumers’ financial needs evolve. Offering a broader suite of financial products can deepen customer loyalty and drive new revenue streams. For example, growing adoption of merchant payments could enable preapproved lending, while insurance products could be bundled with loans or transport-related transactions. As users engage with a wider range of services, mobile money can play a greater role in advancing both economic growth and individual financial well-being.