Is Tat Hong Equipment Service (HKG:2153) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that (HKG:2153) does use debt in its business. But the real question is whether this debt is making the company risky.

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

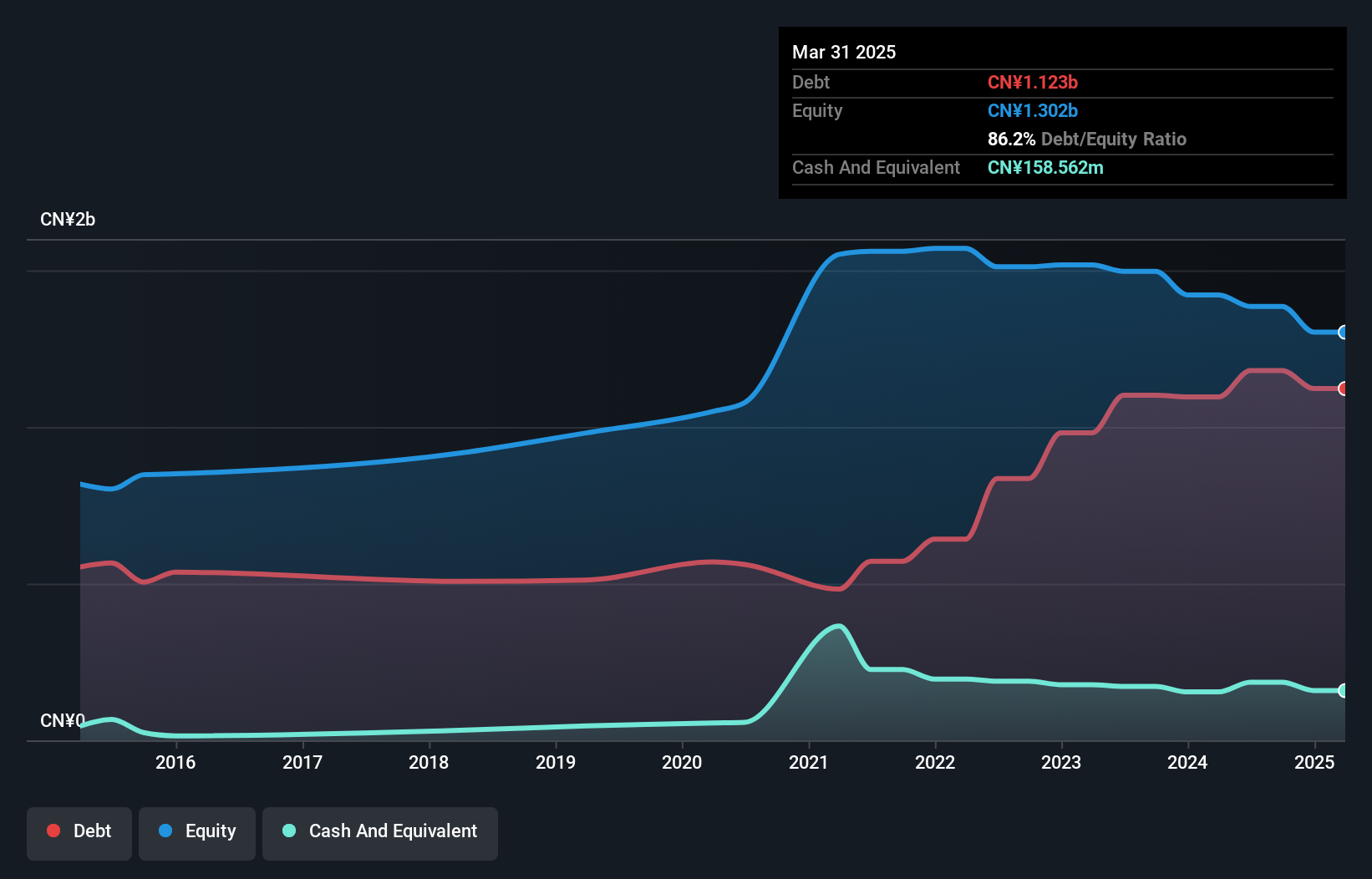

The chart below, which you can click on for greater detail, shows that Tat Hong Equipment Service had CN¥1.12b in debt in March 2025; about the same as the year before. However, it also had CN¥158.6m in cash, and so its net debt is CN¥964.1m.

The latest balance sheet data shows that Tat Hong Equipment Service had liabilities of CN¥1.10b due within a year, and liabilities of CN¥701.3m falling due after that. Offsetting this, it had CN¥158.6m in cash and CN¥900.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥745.6m.

This deficit is considerable relative to its market capitalization of CN¥1.05b, so it does suggest shareholders should keep an eye on Tat Hong Equipment Service's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Tat Hong Equipment Service will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

View our latest analysis for Tat Hong Equipment Service

In the last year Tat Hong Equipment Service had a loss before interest and tax, and actually shrunk its revenue by 7.0%, to CN¥635m. That's not what we would hope to see.

Over the last twelve months Tat Hong Equipment Service produced an earnings before interest and tax (EBIT) loss. To be specific the EBIT loss came in at CN¥42m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. Another cause for caution is that is bled CN¥33m in negative free cash flow over the last twelve months. So to be blunt we think it is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt , right now.

Discover if Tat Hong Equipment Service might be undervalued or overvalued with our detailed analysis, featuring

Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.