When going got tough for equity investors, how trusted financial advisors made it easy and rewarding - The Economic Times

In September last year, a 56-year-old retiree from Mumbai reached out to her financial planner, Santosh Joseph, CEO of Germinate Investor Services. The former public sector bank employee wanted to invest in equities for the first time. She had parked her money in fixed deposits (FD) for most part of her working life and now wanted to get a taste of equities.

When March 2025 lows came, she was distraught. Her portfolio had lost 15% in just three months. She regretted her decision, thinking that venturing into equities was akin to gambling and that she ought to have stayed away. However, a call from Joseph changed her mind—and her fortunes. Ten months later, she has not just recovered her losses, but made a smart profit as well.

Managing Director & Chief Financial Planner, Dilzer Consultants

The power of compounding actually works. Discipline in markets is one of the most underrated, yet powerful, tools for successful investing.

Not having a financial adviser as a sounding board for irrational decision-making.

Fall in portfolio values, uncertainty and lack of direction.

We increased exposure to gold, bonds and equities, where we found gaps in asset allocation, or where monies were waiting on the sidelines for deployment in the markets.

Equity.

Stories like these aren’t rare. As market volatility has tested investor nerves, financial planners have quietly played the role of steady navigators—booking profits, tweaking asset mixes and, most importantly, stopping panic in its tracks.

Between August 2024 and June 2025, the Sensex swung nearly 14,500 points. Bond yields seesawed (but largely fell), and midcap and small-cap stocks corrected. For the average investor, it was a nerve-wracking ride. However, those with experienced financial planners by their side found ways to not just survive, but thrive.

We spoke to several such advisers to understand how smart strategy and steady counsel had made all the difference.

In 2023, when small-cap equity funds were all the rage with investors, with net inflows worth Rs.41,035 crore, Gurugram-based financial adviser Ashish Chadha sent out a note to his investors to go slow on equities.

Chadha, Director of Chadha Investment Consultant, had stopped recommending them small-cap funds back then. He had even dissuaded them from fresh systematic investment plans (SIP) and, instead, channelled their savings to government securities and gold funds.

“The year 2023 was bad for business,” says Chadha, referring to the contrarian call, when everyone wanted a piece of equities as the S&P BSE Sensex went up by 20% that year.

Founder, Ladder7 Financial Advisories

40% in equity; 35% debt; 15% hybrid/multi-asset funds; 10% gold and silver.

Continue with your monthly investments in spite of turbulence in the markets.

I have always followed strategic asset allocation; never invested tactically to take advantage of the markets.

Took advice to invest in gold and silver.

Having witnessed an impressive influx of more than Rs.41,000 crore, small-cap funds posted more inflows than outflows that year.

At the time, Chadha’s only recommendation in equity was large-cap funds and Nifty Next50 index passive funds. A year later, his investors not just recovered losses, but made a smart profit as well. “Typically, a 60% allocation in equities is ideal. Going slow in mid caps and equities in 2023 and much of 2024 helped our clients’ allocation to equities come back to around 60%,” says Chadha.

The ongoing SIPs aside, investors and advisers also look for opportune moments to step up their investments. This is not market timing, but the point where, after a persistent fall in the markets, it seems reasonably safe to put in a small lump sum. On 4 March, when the Sensex hit a low of 72,989 points, smart advisers saw little downside from thereon and nudged investors to step up their equity investments.

Investors often panic when the market falls. However, they need to remember that it recovers as well.

Managing Director & Chief Executive Officer, Etica Wealth

Investing in a PSU fund in August 2020. My four-year SIP return: 56% (compounded).

I just show them my family’s portfolio. We either swim together or sink together.

The problem is most investors don’t even follow ‘Plan A’ properly. Brian Feroldi, a US based wealth professional, once said, “The best investment plan for you isn’t based on some formula. It’s the one you’ll actually stick with when markets are crashing.”

Goal-based investing discussions. Let’s try and solve the real money problem of our investors. I’m not interested in market discussions.

Gajendra Kothari, Managing Director & Chief Executive Officer, Etica Wealth, a Mumbai-based distribution firm, advised his clients to resume lump-sum investments in equities that day and continued reinforcing his message throughout the week.

“We invest a lot via SIPs. So most of my clients have been investing regularly, but many don’t do it through SIPs. We dug into our database and found those who don’t, and reached out to convince them that it was a good time to get back in,” says Kothari.

He adds that his firm deployed nearly Rs.10 crore that week between fresh inflows, additional lump-sum top-ups and switches from liquid funds. Of this, Rs.2.26 crore came through fresh purchases and Rs.5 crore via 234 additional purchase transactions.

Elsewhere, Dilshad Billimoria, Managing Director and Chief Financial Planner at Dilzer Consultants, a Sebi-registered investment advisory firm, increased the time period of her clients’ systematic transfer plans (STP), in 2024, as equity markets were going up. The STP facility helps transfer money from liquid or short-term debt funds to equity mutual funds. It helps investors with a lump sum in hand to deploy money steadily into equities. “If somebody had an STP program of 12 weeks, we increased it to 20,” she says. Billimoria’s firm also dug deep into the clients’ portfolios to identify non-performers and took advantage of the rising markets to consolidate.

Even if your SIPs are on, there are special situations that may require deft handling. If these come up amidst market mayhem and global uncertainty, it could cloud your judgement. Here’s where a guiding hand is reassuring. Suresh Sadagopan, Founder of Ladder7 Financial Advisories, tells us about a client who was a senior executive in her company, but was constantly stretched financially on account of multiple loans and high cost of her children’s education. In February, at the height of the US trade tariff uncertainty, Sadagopan realised that she had a lot of employee stock options from her US-based company that were lying in a US-based depository account. Sadagopan said that the company itself wasn’t in a great shape. “We sold a small portion of her US shares to close some of her loans. We retired quite a few of her loans so that a larger portion of her regular salary here could be directed towards savings,” says Sadagopan.

Director, Chadha Investment Consultant

Not watching social media and TV as it messes up your asset allocation.

Listen.

Operation Sindoor and the Israel-Iran conflict.

Medium risk. If price is cheap, it turns high.

Discussing portfolios over a third whiskey at a party.

In another instance, according to Sadagopan, a client who retired in November 2024 got a large sum as retiral benefit, including the provident fund and gratuity. Equity markets had already started to fall by then; the Sensex had fallen by 8% between the peak of September and November-end. While regular income needs were to be met from debt investments, Sadagopan had to ensure longevity of the corpus by investing a chunk in equities. A large lump sum (part of retiral benefits) is usually invested through STPs. The question was by what time.

Here, he says, his firm initiated STPs of 20-24 weeks, instead of the usual 10-12 weeks. “It worked out quite well. The STPs were started when equity markets were at relatively lower points. We also put some money in gold and silver assets.”

If you have invested wisely and are continuing with your SIPs, what does a financial adviser bring to the table?

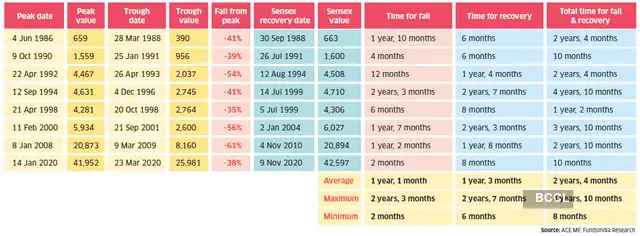

Most advisers we spoke to said that they didn’t need to do anything with a majority of their clients. Sadagopan adds that none of his clients asked him to stop the SIPs. He says that volatile periods like the one prevalent since September 2024 don’t really call for significant action because “we generally build a high margin of safety when we make financial plans”. Besides, it’s a fact that what goes down, eventually comes up (see table).

CEO, Germinate Investor Services

These are extremely important and relevant. Just beware of the position sizing.

Over-confidence and over-expectation.

Not starting to invest early.

Being able to afford what you want to do with your time and yourself. Everything else transcends this.

During a sharp correction, say, 10% or more, within a short period of time.

“Knowing that their basics are covered helps clients stay invested with more confidence,” says Rohit Shah, Founder & CEO, GYR Financial Planners. In the past 10 months, Shah says none of his clients have stopped their SIPs, even as volatility has surged. Sometimes, however, volatility provides tactical opportunities. Shah recollects a client for whom he had already planned, sometime last year, to deploy money in mid-cap funds once valuations became attractive, over six months. But when mid- and small-cap indices dropped sharply in late 2024, Shah reached out with a suggestion: “Let’s prepone the next few instalments.”

Money was already parked in liquid funds and an STP was on. “Based on our analysis, that segment was offering good value,” he recalls. The client agreed, and they redeployed the capital at a lower NAV (net asset value).

Founder & CEO, Getting You Rich Financial Planners

Faith in the future, patience with results, and disciplined investing.

A behaviour firefighter, stepping in to manage emotions and guide decisions.

‘Love’ that a family holds for generations to come.

Predicting a market correction that’ll last throughout 2025 due to Operation Sindoor and US President Donald Trump’s tariffs.

If you’re in the accumulation phase, what happens in the next six months won’t matter.